Cash Buyer vs Mortgaged Investor: Who Wins in 2025? – Regional Comparisons Across the UK

In a high-interest, high-inflation environment, property investors are asking a vital question in 2025: “Is it better to buy with cash or leverage using a mortgage?” The answer isn't as simple as it once was. With mortgage rates still above historical averages, regional yield disparities, and shifting market conditions, the right strategy could depend largely on where you're investing and what your financial goals are.

This article dives deep into the pros and cons of cash buying vs mortgaged investing in 2025, and how regional performance across the UK can tilt the scales one way or the other.

The 2025 Financing Landscape: Setting the Scene

While inflation has cooled compared to 2023 peaks, interest rates remain elevated compared to the ultra-low environment of the 2010s. Average buy-to-let mortgage rates in mid-2025 hover between 5.2% and 6.0%, making borrowing more expensive—and eroding profits in lower-yield areas.

On the flip side, cash buyers have re-entered the market strongly, buoyed by:

Inheritance and equity release

Disillusionment with volatile equities

A desire for hassle-free income and capital stability

With nearly 38% of all property purchases in Q2 2025 made in cash (HM Land Registry), the competition between cash-rich investors and leveraged landlords is heating up.

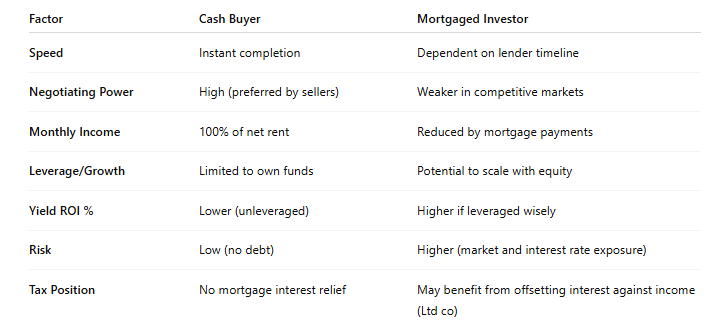

Pros & Cons: Cash vs Mortgaged Investors in 2025

Regional Comparisons: Where the Strategies Diverge

Let’s compare how cash vs mortgage plays out in key UK regions in 2025.

North West – e.g. Liverpool, Preston, Blackpool

The North West remains a powerhouse for yield-driven investors, with major cities like Liverpool and affordable coastal areas such as Blackpool attracting both domestic and overseas buyers. The region offers some of the UK’s highest gross rental yields, combined with relatively low entry prices. This creates opportunities for both cash buyers looking for strong passive income, and leveraged investors seeking capital efficiency. However, with mortgage rates still high, the margin for error is slim for those using finance.

Average property price: £135,000–£180,000

Average gross rental yield: 7–9%

Net yield for mortgaged investors (75% LTV @ 5.8% interest): ~4.5–5.2%

Cash buyer yield (net): 6–7%

Winner: Tied.

Mortgage investors can outperform if they secure a high-yielding unit. But cash buyers benefit from strong passive income without rate risk. Popular for long-term cash-rich landlords.

South East – e.g. Reading, Crawley, Maidstone

In the South East, high property prices and modest rental returns present a more challenging landscape for mortgaged investors. With borrowing costs still elevated, monthly net profits are slim—often barely exceeding mortgage payments. In this environment, cash buyers are able to sidestep the squeeze entirely, maintaining a reliable income stream while also benefitting from the region’s long-term capital growth potential.

Average property price: £300,000–£400,000

Average gross rental yield: 4–5%

Net yield for mortgaged investors (75% LTV): ~2.5–3.2%

Cash buyer yield (net): 3.8–4.2%

Winner: Cash buyer.

Mortgage repayments eat too far into rental profits in the South East unless long-term capital appreciation is the goal. Cash buyers dominate here for passive yield and simplicity.

Midlands – e.g. Nottingham, Leicester, Derby

The Midlands continues to be a balanced and reliable option for landlords in 2025. With mid-level property prices and healthy tenant demand, cities like Nottingham and Leicester offer a mix of rental yield and growth potential. Investors using leverage can still secure solid returns here—particularly on HMOs or newly refurbished units—while cash buyers enjoy respectable yields without interest-rate exposure. This makes the Midlands a sweet spot for both strategies.

Average property price: £190,000–£230,000

Average gross rental yield: 5.5–7%

Net yield for mortgaged investors: ~3.8–4.5%

Cash buyer yield (net): 5.2–5.8%

Winner: Marginally mortgaged investor (for growth), but cash still strong.

Leverage enables portfolio scaling in the Midlands where yields support it, but cash remains solid for income investors.

London

In London, high purchase prices and low yields make mortgaged buy-to-let increasingly unviable for most landlords in 2025. The cost of borrowing often exceeds the net income generated by rent, especially in Zones 1–3. Cash buyers, however, still operate here—especially in the prime and super-prime segments—often focused more on asset preservation and long-term appreciation than short-term rental income. This skews the field toward those with capital rather than those seeking income via finance.

Average property price: £450,000–£650,000

Average gross rental yield: 3–4%

Net yield for mortgaged investors: Often <2%

Cash buyer yield (net): 2.5–3.2%

Winner: Cash buyer (for UHNW investors), but risky for yield-driven buyers.

London makes little sense for mortgaged landlords in 2025 unless betting on long-term appreciation. Cash-rich international buyers dominate prime postcodes.

Scotland – e.g. Aberdeen, Dundee, Glasgow

Scotland presents an often overlooked opportunity for both types of investor. Cities like Glasgow and Dundee offer strong yields, affordable entry points, and increasing demand from students and professionals alike. Meanwhile, Aberdeen—though more volatile due to its energy-sector exposure—is beginning to stabilise with the growth of green energy projects. Investors using leverage can still secure healthy cash flow in this region, but cash buyers are just as active given the low acquisition costs.

Average property price: £140,000–£200,000

Average gross rental yield: 6–8%

Net yield for mortgaged investors: 4.2–5.5%

Cash buyer yield (net): 5.8–6.5%

Winner: Mortgaged investors (for yield chasers).

If rates drop or rents rise, mortgage strategies in Scotland could outperform. But entry-level cash purchases remain attractive.

Strategy Snapshot: When to Use Each Approach

✅ Cash Buying is Best For:

Investors over 55 with pension/lump sum income

Buyers targeting high-yield, low-maintenance units

Those wanting no debt, no risk, and faster deals

Lower-value regions (North West, Scotland, Wales)

✅ Mortgaged Investing is Best For:

Buyers with equity release or growing portfolios

Areas where capital growth is the long-term goal

Sophisticated investors using Ltd company tax wrappers

Regions with solid yields and lower prices (Midlands, some of North)

What Happens If Rates Fall in 2026?

Should the Bank of England cut rates in late 2025 or early 2026, mortgaged investors may reclaim dominance, especially in mid-yield markets. Remortgaging or refinancing could unlock previously unviable deals and boost cash flow. However, until that happens, the risk-adjusted return for cash buyers is stronger in many regions.

Conclusion: Who Wins in 2025?

In a word: It depends. But broadly speaking:

Cash buyers dominate in the South East, London, and coastal towns like Anglesey, Lytham St Annes, and parts of Cornwall.

Mortgaged investors remain competitive in yield-heavy areas like Liverpool, Preston, parts of Scotland and the Midlands—as long as yields outweigh interest costs.

Both strategies have merit, and savvy investors in 2025 often combine both—using cash to acquire undervalued deals and leveraging when the returns justify the risk.

Ready to Analyse Your Best Option?

At Residential Estates, we help investors build tailored portfolios across the UK based on their financing profile, risk appetite, and yield targets. Whether you're cash-rich or loan-leveraging, we’ll help you identify the best markets and the right opportunities for 2025 and beyond.

Book a strategy call today and make your money work smarter.